10. Job Search#

GPU

This lecture was built using a machine with JAX installed and access to a GPU.

To run this lecture on Google Colab, click on the “play” icon top right, select Colab, and set the runtime environment to include a GPU.

To run this lecture on your own machine, you need to install Google JAX.

In this lecture we study a basic infinite-horizon job search problem with Markov wage draws

Note

For background on infinite horizon job search see, e.g., DP1.

The exercise at the end asks you to add risk-sensitive preferences and see how the main results change.

In addition to what’s in Anaconda, this lecture will need the following libraries:

!pip install quantecon

Show code cell output

Requirement already satisfied: quantecon in /home/runner/miniconda3/envs/quantecon/lib/python3.12/site-packages (0.8.0)

Requirement already satisfied: numba>=0.49.0 in /home/runner/miniconda3/envs/quantecon/lib/python3.12/site-packages (from quantecon) (0.60.0)

Requirement already satisfied: numpy>=1.17.0 in /home/runner/miniconda3/envs/quantecon/lib/python3.12/site-packages (from quantecon) (1.26.4)

Requirement already satisfied: requests in /home/runner/miniconda3/envs/quantecon/lib/python3.12/site-packages (from quantecon) (2.32.3)

Requirement already satisfied: scipy>=1.5.0 in /home/runner/miniconda3/envs/quantecon/lib/python3.12/site-packages (from quantecon) (1.13.1)

Requirement already satisfied: sympy in /home/runner/miniconda3/envs/quantecon/lib/python3.12/site-packages (from quantecon) (1.13.2)

Requirement already satisfied: llvmlite<0.44,>=0.43.0dev0 in /home/runner/miniconda3/envs/quantecon/lib/python3.12/site-packages (from numba>=0.49.0->quantecon) (0.43.0)

Requirement already satisfied: charset-normalizer<4,>=2 in /home/runner/miniconda3/envs/quantecon/lib/python3.12/site-packages (from requests->quantecon) (3.3.2)

Requirement already satisfied: idna<4,>=2.5 in /home/runner/miniconda3/envs/quantecon/lib/python3.12/site-packages (from requests->quantecon) (3.7)

Requirement already satisfied: urllib3<3,>=1.21.1 in /home/runner/miniconda3/envs/quantecon/lib/python3.12/site-packages (from requests->quantecon) (2.2.3)

Requirement already satisfied: certifi>=2017.4.17 in /home/runner/miniconda3/envs/quantecon/lib/python3.12/site-packages (from requests->quantecon) (2024.8.30)

Requirement already satisfied: mpmath<1.4,>=1.1.0 in /home/runner/miniconda3/envs/quantecon/lib/python3.12/site-packages (from sympy->quantecon) (1.3.0)

We use the following imports.

import matplotlib.pyplot as plt

import quantecon as qe

import jax

import jax.numpy as jnp

from collections import namedtuple

jax.config.update("jax_enable_x64", True)

10.1. Model#

We study an elementary model where

jobs are permanent

unemployed workers receive current compensation

the horizon is infinite

an unemployment agent discounts the future via discount factor

10.1.1. Set up#

At the start of each period, an unemployed worker receives wage offer

To build a wage offer process we consider the dynamics

where

We then discretize this wage process using Tauchen’s method to produce a stochastic matrix

Successive wage offers are drawn from

10.1.2. Rewards#

Since jobs are permanent, the return to accepting wage offer

The Bellman equation is

We solve this model using value function iteration.

10.2. Code#

Let’s set up a namedtuple to store information needed to solve the model.

Model = namedtuple('Model', ('n', 'w_vals', 'P', 'β', 'c'))

The function below holds default values and populates the namedtuple.

def create_js_model(

n=500, # wage grid size

ρ=0.9, # wage persistence

ν=0.2, # wage volatility

β=0.99, # discount factor

c=1.0, # unemployment compensation

):

"Creates an instance of the job search model with Markov wages."

mc = qe.tauchen(n, ρ, ν)

w_vals, P = jnp.exp(mc.state_values), jnp.array(mc.P)

return Model(n, w_vals, P, β, c)

Let’s test it:

model = create_js_model(β=0.98)

model.c

1.0

model.β

0.98

model.w_vals.mean()

Array(1.34861482, dtype=float64)

Here’s the Bellman operator.

@jax.jit

def T(v, model):

"""

The Bellman operator Tv = max{e, c + β E v} with

e(w) = w / (1-β) and (Ev)(w) = E_w[ v(W')]

"""

n, w_vals, P, β, c = model

h = c + β * P @ v

e = w_vals / (1 - β)

return jnp.maximum(e, h)

The next function computes the optimal policy under the assumption that

The policy takes the form

Here

@jax.jit

def get_greedy(v, model):

"Get a v-greedy policy."

n, w_vals, P, β, c = model

e = w_vals / (1 - β)

h = c + β * P @ v

σ = jnp.where(e >= h, 1, 0)

return σ

Here’s a routine for value function iteration.

def vfi(model, max_iter=10_000, tol=1e-4):

"Solve the infinite-horizon Markov job search model by VFI."

print("Starting VFI iteration.")

v = jnp.zeros_like(model.w_vals) # Initial guess

i = 0

error = tol + 1

while error > tol and i < max_iter:

new_v = T(v, model)

error = jnp.max(jnp.abs(new_v - v))

i += 1

v = new_v

v_star = v

σ_star = get_greedy(v_star, model)

return v_star, σ_star

10.3. Computing the solution#

Let’s set up and solve the model.

model = create_js_model()

n, w_vals, P, β, c = model

v_star, σ_star = vfi(model)

Starting VFI iteration.

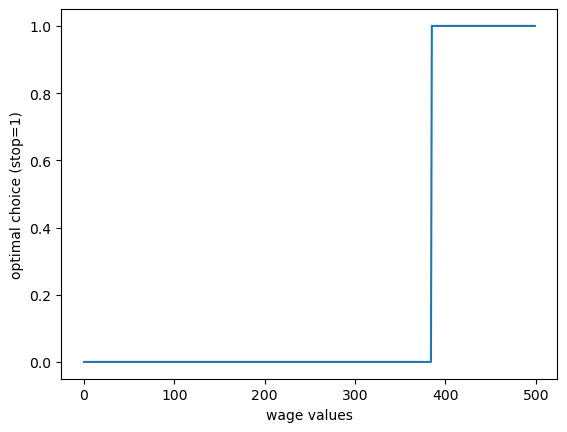

Here’s the optimal policy:

fig, ax = plt.subplots()

ax.plot(σ_star)

ax.set_xlabel("wage values")

ax.set_ylabel("optimal choice (stop=1)")

plt.show()

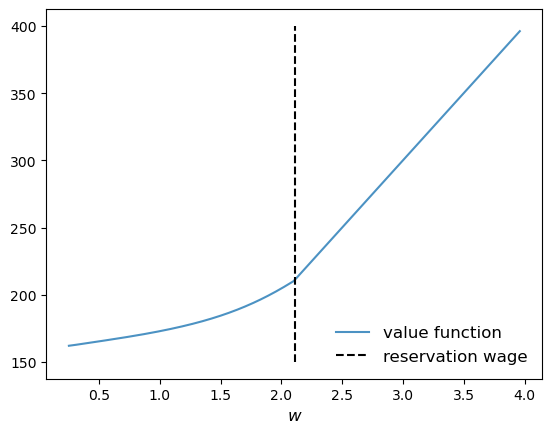

We compute the reservation wage as the first

stop_indices = jnp.where(σ_star == 1)

stop_indices

(Array([385, 386, 387, 388, 389, 390, 391, 392, 393, 394, 395, 396, 397,

398, 399, 400, 401, 402, 403, 404, 405, 406, 407, 408, 409, 410,

411, 412, 413, 414, 415, 416, 417, 418, 419, 420, 421, 422, 423,

424, 425, 426, 427, 428, 429, 430, 431, 432, 433, 434, 435, 436,

437, 438, 439, 440, 441, 442, 443, 444, 445, 446, 447, 448, 449,

450, 451, 452, 453, 454, 455, 456, 457, 458, 459, 460, 461, 462,

463, 464, 465, 466, 467, 468, 469, 470, 471, 472, 473, 474, 475,

476, 477, 478, 479, 480, 481, 482, 483, 484, 485, 486, 487, 488,

489, 490, 491, 492, 493, 494, 495, 496, 497, 498, 499], dtype=int64),)

res_wage_index = min(stop_indices[0])

res_wage = w_vals[res_wage_index]

Here’s a joint plot of the value function and the reservation wage.

fig, ax = plt.subplots()

ax.plot(w_vals, v_star, alpha=0.8, label="value function")

ax.vlines((res_wage,), 150, 400, 'k', ls='--', label="reservation wage")

ax.legend(frameon=False, fontsize=12, loc="lower right")

ax.set_xlabel("$w$", fontsize=12)

plt.show()

10.4. Exercise#

Exercise 10.1

In the setting above, the agent is risk-neutral vis-a-vis future utility risk.

Now solve the same problem but this time assuming that the agent has risk-sensitive preferences, which are a type of nonlinear recursive preferences.

The Bellman equation becomes

When

Solve the model when

Try to interpret your result.

You can start with the following code:

RiskModel = namedtuple('Model', ('n', 'w_vals', 'P', 'β', 'c', 'θ'))

def create_risk_sensitive_js_model(

n=500, # wage grid size

ρ=0.9, # wage persistence

ν=0.2, # wage volatility

β=0.99, # discount factor

c=1.0, # unemployment compensation

θ=-0.1 # risk parameter

):

"Creates an instance of the job search model with Markov wages."

mc = qe.tauchen(n, ρ, ν)

w_vals, P = jnp.exp(mc.state_values), mc.P

P = jnp.array(P)

return RiskModel(n, w_vals, P, β, c, θ)

Now you need to modify T and get_greedy and then run value function iteration again.

Solution to Exercise 10.1

RiskModel = namedtuple('Model', ('n', 'w_vals', 'P', 'β', 'c', 'θ'))

def create_risk_sensitive_js_model(

n=500, # wage grid size

ρ=0.9, # wage persistence

ν=0.2, # wage volatility

β=0.99, # discount factor

c=1.0, # unemployment compensation

θ=-0.1 # risk parameter

):

"Creates an instance of the job search model with Markov wages."

mc = qe.tauchen(n, ρ, ν)

w_vals, P = jnp.exp(mc.state_values), mc.P

P = jnp.array(P)

return RiskModel(n, w_vals, P, β, c, θ)

@jax.jit

def T_rs(v, model):

"""

The Bellman operator Tv = max{e, c + β R v} with

e(w) = w / (1-β) and

(Rv)(w) = (1/θ) ln{E_w[ exp(θ v(W'))]}

"""

n, w_vals, P, β, c, θ = model

h = c + (β / θ) * jnp.log(P @ (jnp.exp(θ * v)))

e = w_vals / (1 - β)

return jnp.maximum(e, h)

@jax.jit

def get_greedy_rs(v, model):

" Get a v-greedy policy."

n, w_vals, P, β, c, θ = model

e = w_vals / (1 - β)

h = c + (β / θ) * jnp.log(P @ (jnp.exp(θ * v)))

σ = jnp.where(e >= h, 1, 0)

return σ

def vfi(model, max_iter=10_000, tol=1e-4):

"Solve the infinite-horizon Markov job search model by VFI."

print("Starting VFI iteration.")

v = jnp.zeros_like(model.w_vals) # Initial guess

i = 0

error = tol + 1

while error > tol and i < max_iter:

new_v = T_rs(v, model)

error = jnp.max(jnp.abs(new_v - v))

i += 1

v = new_v

v_star = v

σ_star = get_greedy_rs(v_star, model)

return v_star, σ_star

model_rs = create_risk_sensitive_js_model()

n, w_vals, P, β, c, θ = model_rs

v_star_rs, σ_star_rs = vfi(model_rs)

Starting VFI iteration.

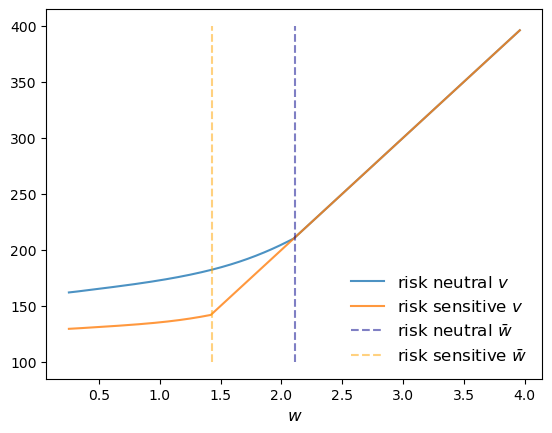

Let’s plot the results together with the original risk neutral case and see what we get.

stop_indices = jnp.where(σ_star_rs == 1)

res_wage_index = min(stop_indices[0])

res_wage_rs = w_vals[res_wage_index]

fig, ax = plt.subplots()

ax.plot(w_vals, v_star, alpha=0.8, label="risk neutral $v$")

ax.plot(w_vals, v_star_rs, alpha=0.8, label="risk sensitive $v$")

ax.vlines((res_wage,), 100, 400, ls='--', color='darkblue',

alpha=0.5, label=r"risk neutral $\bar w$")

ax.vlines((res_wage_rs,), 100, 400, ls='--', color='orange',

alpha=0.5, label=r"risk sensitive $\bar w$")

ax.legend(frameon=False, fontsize=12, loc="lower right")

ax.set_xlabel("$w$", fontsize=12)

plt.show()

The figure shows that the reservation wage under risk sensitive preferences (RS

This makes sense – the agent does not like risk and hence is more inclined to accept the current offer, even when it’s lower.